Here's how it works: You gain access to a credit line based on your age, current interest rates, and home value. You can then draw funds as needed, paying interest only on the amount you use. This flexibility is a major advantage for retirees who want to maintain control over their finances.

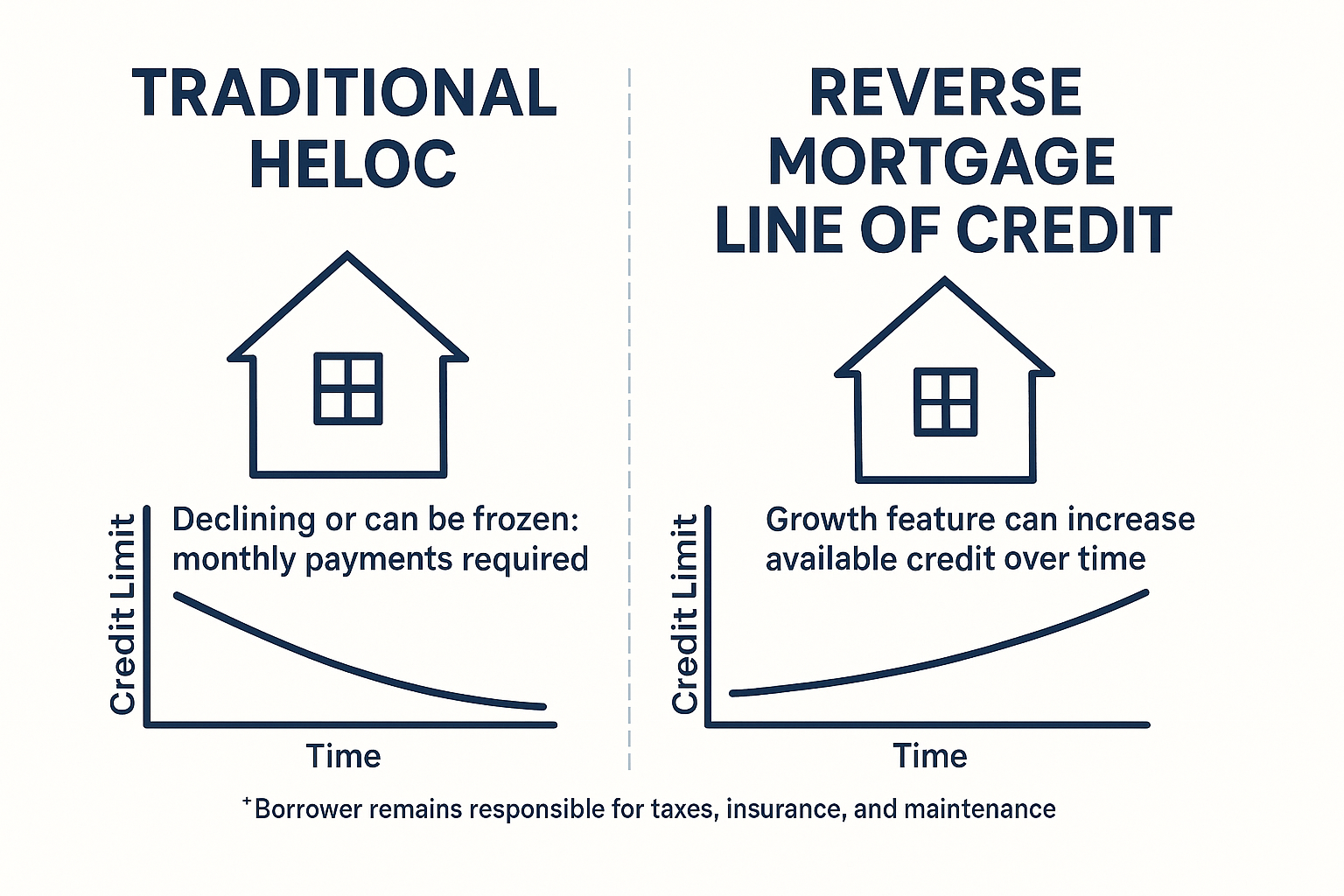

But the real magic lies in its growth potential. The unused portion of your credit line grows annually at a rate equal to the loan's interest rate plus the mortgage insurance premium, currently totaling approximately 6.50% annually as of 2025.

Imagine establishing a $350,000 line of credit and not using it immediately. After five years, it could grow to over $516,000, and after ten years, more than $714,000! This growth acts as a hedge against inflation and ensures you have increasing access to funds as you age.

What is a Traditional HELOC?

A traditional HELOC is a revolving credit line secured by your home. You can typically borrow up to 80% of your home's value, minus any existing mortgage balance. During a "draw period" (usually 10-15 years), you can access funds as needed, making interest-only payments (though you can make principal payments too).

However, qualifying for a HELOC can be challenging for retirees. Lenders typically require credit scores in the mid-to-high 600s, stable income verification, and manageable debt-to-income ratios. These requirements can be difficult to meet when your income primarily comes from Social Security, pensions, or retirement account withdrawals.

Additionally, HELOC interest rates are usually variable, tied to the prime rate, meaning your monthly payments can fluctuate. As of 2025, HELOC rates average around 8%, requiring consistent monthly payments regardless of your income situation. After the draw period, the loan enters a repayment phase, potentially leading to significantly higher monthly payments. Plus, lenders can freeze or reduce your credit line during economic downturns, limiting access when you need it most.

Why a Reverse Mortgage Line of Credit is the Better Choice for Retirees

For retirees, the reverse mortgage line of credit offers several key advantages:

- No Mandatory Monthly Payments: This is the biggest draw. You access your home equity without adding to your monthly expenses. This is especially crucial when income is fixed.

- Easier Qualification: Reverse mortgages use a "residual income" assessment, focusing on what remains after essential expenses, rather than strict income verification. This acknowledges the unique financial situation of retirees.

- Credit Line Growth: As mentioned earlier, the unused portion of your credit line grows over time, providing a hedge against inflation and increasing access to funds.

- Market Protection: Unlike HELOCs, federally insured reverse mortgage lines of credit cannot be frozen or reduced by lenders, even during economic downturns. This provides valuable peace of mind.

How a Reverse Mortgage Line of Credit Can Help

A reverse mortgage line of credit can be a powerful tool for addressing various retirement challenges:

- Medical Expenses: Approximately one-third of reverse mortgage borrowers use their funds for medical expenses, allowing them to remain in their homes.

- Cash Flow Management: Avoid tapping retirement accounts during market downturns by using your home equity instead. This "standby" strategy can extend the life of your portfolio.

- Home Maintenance and Improvements: Fund accessibility upgrades, energy-efficient updates, and smart home technology to support aging in place.

- Emergency Preparedness: The guaranteed access to funds provides a safety net for unexpected expenses.

Key Benefits

Here's a summary of the key benefits:

- Financial Flexibility: Make voluntary payments without penalty.

- Tax Advantages: Funds received are loan proceeds, generally not subject to federal income taxes.

- Protection Against Foreclosure: No payment obligations as long as you maintain the property, pay taxes and insurance, and live in the home.

- Estate Planning Benefits: Heirs are protected against owing more than the home's value, and any remaining equity belongs to the estate.

The Future of Reverse Mortgages

The reverse mortgage market is projected to grow from $1.79 billion in 2024 to $1.92 billion in 2025, representing a 7.6% compound annual growth rate. This growth reflects increasing awareness and acceptance among seniors and financial professionals. With the HECM lending limit reaching $1,209,750 for 2025, homeowners with higher-value properties have even greater access to funds.

Furthermore, technology is transforming the industry, with digital solutions and AI-powered customer service making the process more accessible and user-friendly.

Is a Reverse Mortgage Line of Credit Right for You?

While a reverse mortgage line of credit offers significant advantages, it's crucial to consult with a financial advisor to determine if it's the right fit for your individual circumstances. Consider your financial goals, risk tolerance, and long-term care needs.

Ready to explore your options? Contact Linda today to learn more and unlock the potential of your home equity!